FinTech App Design and Development Cost in 2026

The landscape of financial technology (Fintech) is moving faster than a racecar. We are witnessing how the new generation is turning its back on the traditional approach to handling money. According to research, “70% of Gen Z prefer cashless transactions”.

It's no longer about checking your back pocket wallet or checking the balance on a phone. It has transitioned to Artificial Intelligence (AI). People now rely on AI to save, transfer money, and invest in digital assets.

If you have a vision for a new money-transfer app, a unique way to invest, or a digital-only bank, the very first question you likely have is: "How much will a fintech app cost?" A straightforward answer is that it costs a lot.

A simple, scope-limited app might cost $30,000. On the other hand, a large, complex global platform can exceed $ 350,000.

This blog will break down every single dollar. We will examine where the money goes, why some apps cost more than others, and how you can plan your budget without any unexpected expenses.

Why is fintech app development different from other apps?

Developing finance or fintech is way more complicated than building a dream journal, a game, or a new portal app. A fintech app comes with more tech processes than a normal app. Stakes are higher since these apps handle real money from real users. Steep is narrow because users put their life savings in finance apps.

Another reason for this is that user expectations have gone up. Modern-day users will not tolerate an app that is unattractive, complex, or keeps loading.

- Trust is the #1 currency in 2026: If your app crashes every minute, users will think their money is unsafe.

- Stricter Laws & Regulations: Governments keep track of digital finance. Fintech apps nowadays need to follow more rules than they did a few years ago.

- Smart Features: Users expect the app to be "intelligent". They want the app to let them know when they are overspending, when to save, and not just show numbers.

These demands make Fintech apps harder and often more expensive to build, but the potential reward of Fintech is massive.

Understanding fintech app design & development

Building an app can mean a lot of things. It totally depended on the phase of the building process. For some, building means creating from scratch, designing + developing. For others, building means the development phase.

Building an app = UX Designing + Development

For the sake of keeping this guide short, I will explain the cost of fintech design and development together. But before that, you need to understand why fintech app design services and fintech development services charge differently.

1. Fintech app design

Fintech app design means the look of the app. Which is not only about making the app look good; it's more about creating a design that doesn't feel like a burden to use. App design is an art of UX & UI that ensures making an app(product) that feels secure, friendly, and easy to use.

Check out our blog if you are interested to know Top 20 Mobile App Design Agencies in the USA (Reviewed)

Fintech app design: What is it?

- User Experience (UX): User research to find the user's happy path. It focuses on how users are able to send money or do finance in just two or three taps without confusion.

- User Interface (UI): The look of the app. It involves choosing colors, fonts, buttons, and structure that are attractive as well as easy to use.

- Trust & Clarity: Since Fintech is about money. The app design must look secure and professional at the same time. If an app looks lacklustre, users won't trust the product with their savings.

2. Fintech app development

Fintech app development is the process of coding a finance app and making it usable on phones. The development actually makes the app alive by coding both the front-end & back-end together. Simply, the development is that "engine" under the hood of the racecar.

Development is a complex process that requires a team of talented individuals, developers, engineers, and more.

Fintech app development: What is it?

- Front-end: It makes the app look the same as the design; the front-end ensures the finance app looks and feels the same as the design. When a user taps on the "Send" button, the front-end sends that command to the "back-end".

- Back-end: It makes the app functional. It communicates with the user accounts and the bank’s servers. Checks bank reconciliation, records, and transactions.

- Security: It is the most important part of fintech development. Developers use encryption and biometrics (FaceID or fingerprints) to keep your money safe. Fintech security doesn't stop here; developers have to ensure the app is impenetrable from cyberattacks and hackers every day.

What is the average Fintech app building cost?

The average fintech app building cost is between $30,000 - $350,000. However, this price depends on the cost of its design and development. Meaning both of the stages of designing and building cost differently. Doing them separately costs higher and the process is slower.

Pro tip: Getting fintech design agencies that provide both of the services in one package is the smart choice.

Scope is the biggest factor of cost difference in developing a fintech app.

The scope (size, features) of fintech determines how much it would cost to build. A good example is a shopping mall, building a small shop, or a giant shopping mall. They both serve people, but the smaller one costs less than the other one.

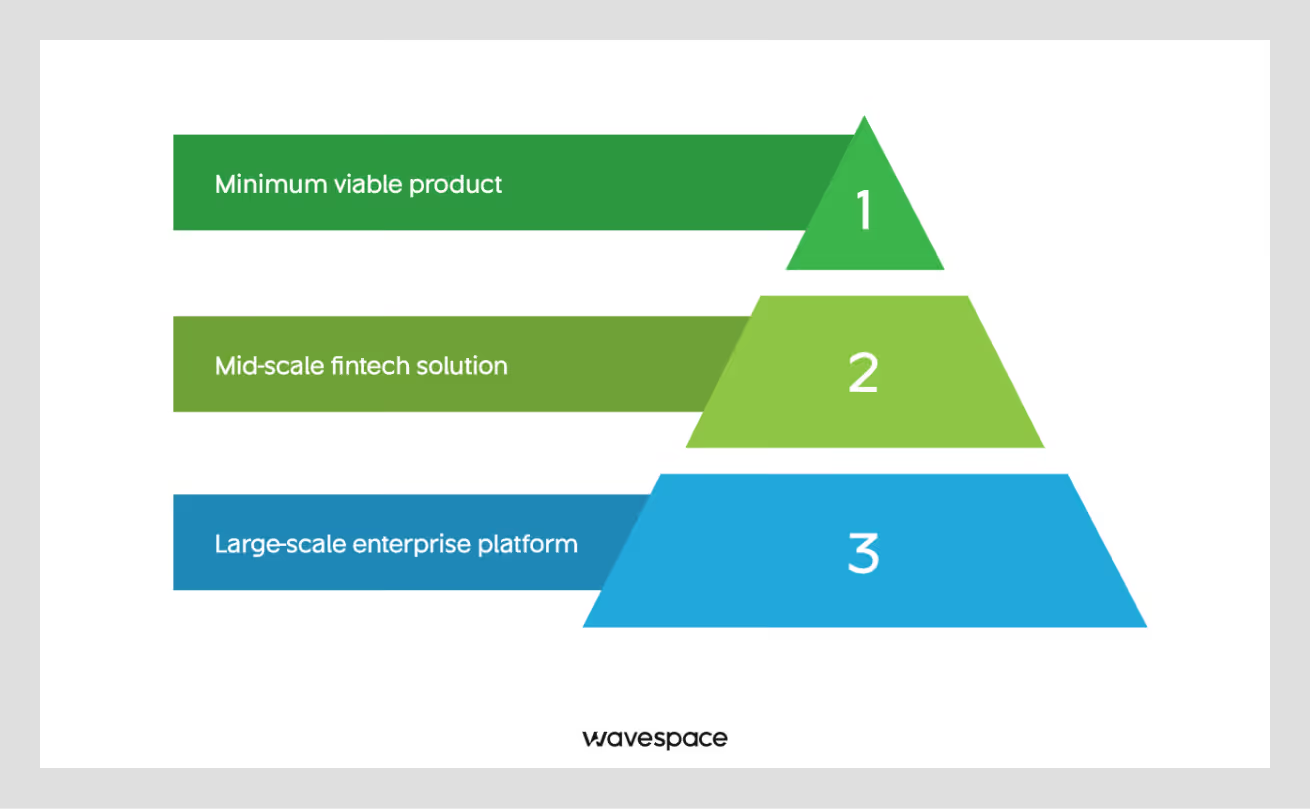

Fintech app development can be split into three levels:

1. Minimum Viable Product (MVP)

Fintech MVP is an ideal way to build and test the product without pouring the whole budget. There is a perception in the industry that MVP is an "unfinished" app, which is wrong.

In truth, an MVP is a minimal feature-focused version of your app. It comes with core features and access to launch the product. The Fintech MVP app is perfect for startups trying to make a buzz in the finance industry.

Note: MVP does not come with every heavy-hitting feature, but it comes with core functions for a jumpstart. It is the smartest way to launch because it lowers your risk.

Estimated cost: $30,000 - $70,000

Core features included

- Secure sign-up and Login methods: Including verifying the user (Identity Verification). Preventing fake accounts from being made.

- Dashboard: A clean, simple dashboard screen. Users can check their balance and recent transactions.

- Transactions: Ability to complete the app's core functionalities. Sending money to a friend, requesting money, or buying a stock. However, in MVP, transactions are limited to one or two payment methods in order to keep development costs down.

- Admin Panel: A website (for the admins) to see an overview, manage basic admin stuff, and support issues.

- Push Notifications: Simple alerts to tell a user "Money Sent" or "Money Received".

2. Mid-scale fintech solution

A mid-scale app is what most people think when talking about app building. It is a standard app with fully functioning features. Professional complete look, works smoothly on both iPhones (iOS) and Android. It's a full app that connects to other bank services to offer more financial facilities.

Estimated cost: $70,000 - $150,000

Advanced fintech functionalities

- Fully-loaded App: A whole fintech app as a package comes with every functional feature to operate and appeal to different users.

- Advanced Security: Biometric login allows users to access with FaceID or fingerprint. Giving an extra layer of protection. This makes the finance app safer as well as faster for daily transactions.

- Smart Integrations: Connects the fintech app with multiple payment gateways. Such as (PayPal, Stripe, or 3rd-party services) and bank APIs (Plaid, Flinks, and more). Letting users link their bank accounts and transfer money at ease.

- Customer Support Chat: A built-in customer support chat tab. Where users can contact the support team within the app.

- History and Filtering: Advanced transaction search tools. Let users find transaction data from a specific date (month or year ago).

3. Large-scale enterprise platform

Building an enterprise-level or scaling a fintech project is expensive. The purpose of the large-scale is to handle millions of users at the same time. Like other banking apps such as Chase, Revolut, or Robinhood.

Enterprise-level fintech apps are able to withstand millions of users without slowing down. This level of large-scale fintech is different from mid-scale. It is more complex and requires an expert team with previous large-scale experience.

Estimated Cost: $150,000 - $350,000+

High-level scalability and Global reach

- AI Analytics & Personalization: A fintech app uses complex AI algorithms to analyze financial data. Reports about spending habits and provides personal alerts & advice. Such as, "You have spent more than 15% on your monthly expense budget ".

- Multi-Language & Multi-Currency: The app is developed for working in different countries. Supports multiple languages, automatically changes languages, and calculates exchange rates without assistance.

- Advanced Security Protocols: Provides high-level cybersecurity. Fraud detection automatically runs in the background. The system prevents suspicious transactions from happening.

- Blockchain Integration: Lets the fintech app handle crypto. Allowing users a more secure transfer and unchangeable records of ownership.

Cost breakdown by Fintech category

Not all finance apps are the same. Fintech apps all do finance. However, each of them is different with its special features and abilities. A stock trading app is much more complex than a simple loan calculator.

Here is a detailed look at what different types of apps cost in 2026.

Digital Banking and Virtual Bank

Cost: $90,000 - $200,000+

These apps work as an online/virtual bank and try to replace physical bank branches.

Why does it cost this much?

You need to build a system that can create new bank accounts, issue virtual debit cards, process transfers, and track spending categories.

Complexity: High

Developers have to connect to "Banking-as-a-Service" (BaaS) providers, which requires complex programming.

Example: Chime, Nubank, Revolut, Varo, Monzo

Investment and Trading (WealthTech)

Cost: $80,000 - $250,000

These apps let users buy stocks, ETFs, or gold.

Why does it cost this much?

For speed. Stock prices change every moment; within seconds, users make money. Your app needs to show live data without any delay. If this type of app is slow, users lose money.

Complexity: Very High

Developers need to integrate complex tools for charts and graphs.

Example: Robinhood, E*TRADE, Charles Schwab, TD Ameritrade, Fidelity

Insurance Solutions (InsurTech)

Cost: $60,000 - $150,000

These apps help users with insurance. Mainly buying, managing policies, or filing claims (taking photos of accidents).

Why does it cost this much?

For complex logic in the back-end. Insurance apps often need to predict. And calculate risk and price (premiums) automatically based on the user's data.

Complexity: Medium to High

Developers need to work harder. To ensure a system that deals with insurance claims with processing workflows.

Example: Lemonade, Oscar Health, Root Insurance

Cryptocurrency and Web3 wallets

Cost: $100,000 - $300,000+

Crypto apps let users store, send, and swap cryptocurrency, including Bitcoin, Ethereum, and other digital assets.

Why does it cost this much?

Blockchain technology is complicated. More importantly, blockchain developers are rare. Getting a developer onboard who knows how to write "Smart Contracts" (code that runs on the blockchain) is expensive.

Complexity: Extreme

Security is critical and has a high priority focus. To make sure the crypto app is bug-free. Because a minor bug can lead to a security exploit. An exploit can spiral into Irreversible crypto theft.

Example: Coinbase, Binance, MetaMask, Trust Wallet, Kraken

Peer-to-Peer (P2P) Lending apps

Cost: $50,000 - $120,000.

These apps act like a matchmaker for finance. It works as a medium to connect people who need money with people willing to lend it.

Why does it cost this much?

A P2P lending app needs a system to check credit scores automatically and manage the repayment schedule (who owes what and when).

Complexity: Medium

The focus is on legal contracts and automated mathematics.

Example: LendingClub, Prosper, Upstart, Zopa

Key Factors that Influence fintech app budget in 2026

A fintech app budget depends on the scope and complexity of the app. A usual money transferring app would cost less than an app that handles cash in crypto. It’s because different types of fintech apps come with different types of functionalities, features, restrictions, and government compliance.

1. Regulatory compliance and legal fees

Complying with the law is the number one priority for fintech services. Breaking one financial rule will result in a fine, or your app will get shut down by the government.

GDPR, PCI DSS, and SOC2: Safety rules.

- GDPR - General Data Protection Regulation: Protects user privacy (mandatory in Europe).

- PCI DSS - Payment Card Industry Data Security Standard: Required if you handle credit card numbers.

- SOC2 - System and Organization Controls 2: Proves if your company is secure or not.

- Cost impact: You need to pay extra cash to developers for their time to build compliant systems. + You may need to hire external auditors to audit your app.

- Region-specific licenses: Each country has a different set of banking rules for transactions. You may need to pay consultants to assist you with features you are legally allowed to offer.

2. Security infrastructure

Security is the most expensive part of Fintech. But it is necessary because without it, your fintech will get hacked by the wrongdoers. You don’t want that.

- Biometric Authentication and MFA: Multi-factor authentication or MFA adds another layer of security. It uses multiple verification methods (password + token and biometric) to prove it is really you. Implementing these fintech security measures is expensive + takes time.

- End-to-End Encryption: E2EE encrypts transaction data. So even if hackers steal them, they can't read them to harm the user.

- Fraud Detection: You need to use real-time AI and machine learning that observes strange behavior to stop fraud. For example, A user in New York suddenly logs in from Tokyo.

3. Modern tech stack

The tech stack is referred to as a set of technologies & programming languages used to build a piece of tech.

Native vs. Cross-Platform:

- Native: Building two separate apps for the two phone operating systems (Swift for iOS, Kotlin for Android). Developing two apps for separate user phone users is more expensive. Because it requires types of mobile app developers for twice the work.

- Cross-Platform (Flutter/React): Coding once that works on both operating systems. Developing an app with cross-platforming gives better budget control.

Back-end Power (Cloud): Paying subscription/rent for servers on Amazon (AWS) or Microsoft (Azure). You need to pay more over time. Because more users require bigger servers, and bigger servers cost more.

4. 3rd-Party API integrations

Not everything is coded from scratch, though it is possible, but hard-coding everything will put a heavy toll on the budget. Instead, you "subscribe" to libraries from other companies.

- Examples: You pay a fee to use their service that checks credit scores, or a service that verifies ID cards or other fintech services.

- Cost impact: Integrating these takes developer time, and the services themselves often charge a monthly fee.

However, keep in mind that these 3rd-party APIs are not all necessary to build a fintech app. But a Minimal Viable Product must have these integrations.

Minimum required 3rd-Party integrations for a Fintech MVP

5. Advanced AI and Machine Learning features

If you want advanced features that act like an AI financial advisor. You need to integrate AI and Machine Learning. Existing fintech companies prefer self-made AI with total control over data. However, fintech startups rely on AI APIs. It gives them financial freedom.

Custom AI: Building your own AI is very expensive.

API AI: Using existing AI (OpenAI) is cheaper. But you need to pay the development team to connect it to your app securely.

6. Development cost by region

Another major cost factor is the location where you build them. Different locations have different lifestyles and wages. Hourly rates can differ depending on the country or region where an agency/ developer is situated. Regions also impact skill level and demand for developers.

You only go to an automobile repair shop to fix your car. A plumber with a wrench is not the same as a mechanic.

- United States & Canada: $50-$250 per hour

- Western Europe: $80-$150 per hour

- Eastern Europe: $40-$80 per hour

- Southeast Asia: $25-$50 per hour

North America and Western Europe have top-level experienced developers. But they cost a premium price. Eastern Europe and Asia have skilled engineers with lower prices. The price difference can be huge depending on the region. The same fintech product can be made with millions and hundreds of thousands.

For startups, choosing the right region is important. It is best to find something that aligns with your goal and expectations. Getting a good fintech development agency can lower the total cost of the project without sacrificing any quality.

What is the cost of Fintech app design?

Fintech app design costs or fintech UI UX design costs range from $5,000 to $15,000. It costs more because designing a fintech app is not just about making it look pretty. It’s good user design.

In Fintech, "good design" means a UX design prevents users from making mistakes. It ensures accounts don't mistakenly send money to someone else. Good fintech UX design also ensures app use is easy yet feels secure.

Discovery and user persona research

It is a process of getting quantitative and qualitative data before drawing a single line; designers research their target audience.

What they do: They conduct interviews with potential users and all types of stakeholders. Focuses on questioning about the product and intent.

- Who are the audiences?

- Are they teenagers or retirees?

- What problems do they have with their current bank?

Why pay for research: Research provides probable outcomes and prevents you from building features nobody wants.

High-fidelity wireframing and Prototyping

High-fidelity wireframing and prototyping are processes of creating a near-perfect app that mimics the expected product. It is done to create an interactive, polished version application to test its functionality.

Designers create a "clickable" workflow of the app for checking how it feels to use IRL.

- What it is: An app that mimics the real/final app. But it has no code to run or release publicly. It's only for testing what sticks. You can just tap buttons and move between app screens (Go forward, Go backward, etc.).

- Benefit: It’s a safe method to save cash. It helps to finalize the product before coding. It is much easier to fix a design here than to fix an already released app.

Accessibility compliance (WCAG)

Every type of app, fintech, or real estate must be accessible to everyone. Including individuals with disabilities. Such as vision impairments or physical disabilities.

- Obligation: Many countries legally require apps and web services to follow WCAG (Web Content Accessibility Guidelines).

Fintech app design costs this much because these precautionary requirements are required. A good UI UX designer checks all of these and provides them without asking.

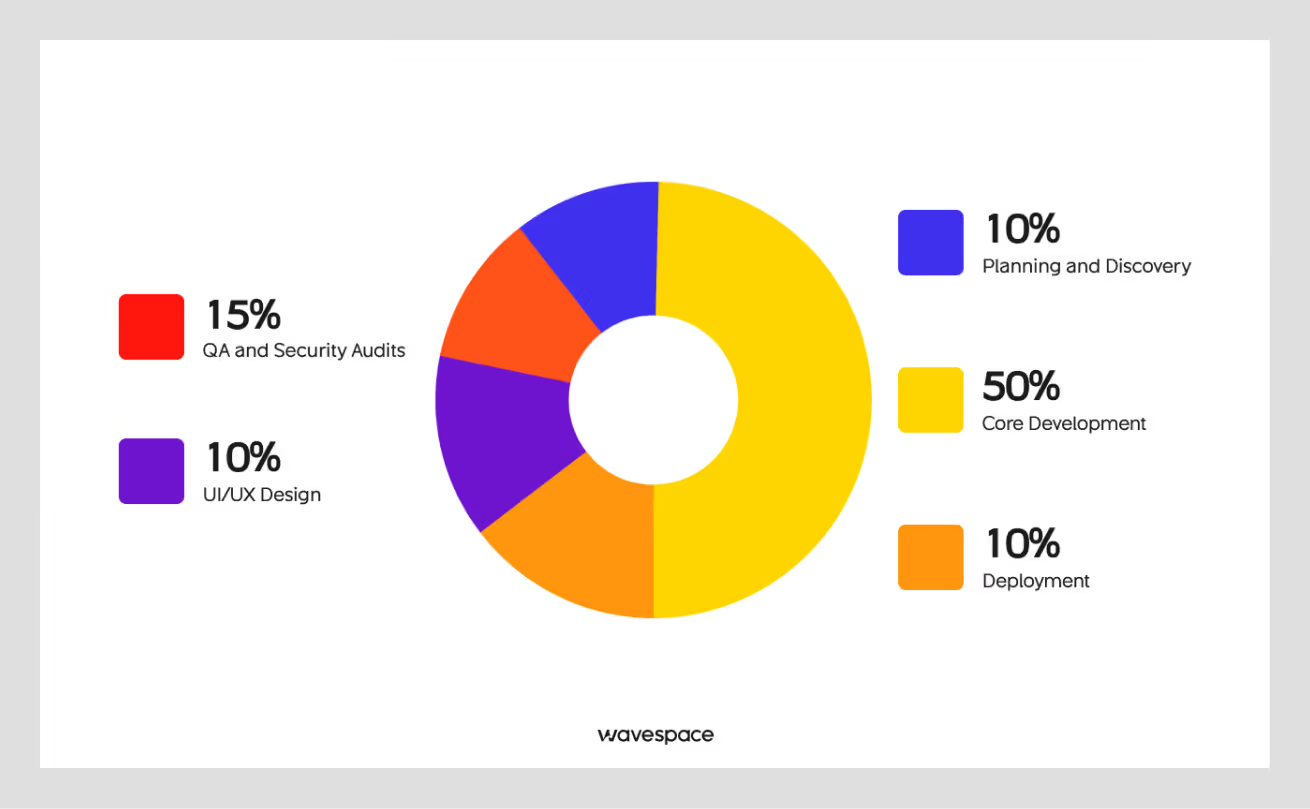

Phase-by-phase development budget allocation of Fintech app

Fintech app building consists of a few phases. It starts with Planning & Discovery, UI/UX Design, Development, QA & Security Audits, and Deployment & Maintenance.

Let’s answer the question, “Where exactly does the money go in fintech development?” Suppose you have a budget of $100,000.

Here is the breakdown of where the money goes.

Planning and Discovery (10% - $10,000)

In this phase, you start to create the blueprint of the fintech app. You determine exactly what your app will be able to do. Create "Functional Specification" documentation. This doc helps developers stop guessing and set a target product to complete. Which saves you money.

UI/UX Design (15% - $15,000)

This phase covers the visual aspect of the app, how it will look, how the app will make the user feel, how the app will prevent the user from making mistakes, and how easy the app will be. The design phase includes the user journey maps. Basic branding (logos, colors), and the final screen designs for every section, screen, and page of the app.

Core Development (50% - $50,000)

Most of the technical work goes into this development phase. After design, development gives life to the app. It makes the app alive and functional.

- Front-end Development: Translate the design of the app. Make what the user sees on the phone.

- Back-end Development: Build the app functionality, secure server, database, and APIs that move money from account to account.

QA and Security Audits (15% - $15,000)

It is a crucial phase. In this phase, the fintech app is rigorously tested to break the app. The purpose of these tests and audits is to find every type of bug, glitch, and security flaw that can harm other users or can be taken advantage of. The testing phase is connected to the development phase.

Every type of error or issue is fixed by the developers.

- QA Testers: They click every button and thoroughly check every corner to find issues/bugs.

- Security Testers: They act as hackers to find vulnerabilities in your security system that can be a safety hazard or lead to a security breach.

Deployment (10% - $10,000)

The launch & maintenance phase. It involves setting up live servers. Submit the app to Apple and Google App Store& Play Store for review before launching to the public. However, work doesn’t stop here. Tech products need constant maintenance and security updates to work smoothly.

Hidden costs and Long-term expenses of the Fintech app

The budget of an app development doesn't cover the post-expense of running the app. Expense doesn’t stop when you launch your fintech app. Just like a car needs gas, fuel, oil changes, and regular checkups, the same thing goes for apps. It needs updates, security patches, bug fixes, and server maintenance.

Annual maintenance and support

Tech items & software degrade over a period of time. Specifically, because smartphones get updated (like iOS 26 or Android 17) and new specs are launched in the market every year. Every update comes with new security measures. Apps need to be updated to support the new phones and comply with major updates for paradigm shifts.

Rule of thumb for app maintenance:

Expect to spend 20% to 40%+ (depending on complexity) of the original development cost every year. Sometimes, providing support and maintenance can be double the development cost. However, for apps, if the building cost is $100k, then set a budget of $20k/year for a smooth ride.

Marketing and user acquisition

Building the best MVP app is not enough. You can build the best app with fully-loaded features, but that won’t guarantee downloads. You need to get your words out. You need to tell people about your app. For this, you need a separate budget for:

- Social Media Ads

- Influencer Marketing

- App Store Optimization (ASO)

Scaling infrastructure as you grow

Fewer users cost less money to maintain. If you have 1000 users, the server bill might be in hundreds. But when you’ve 100,000 users, it’d bill you thousands. Providing support for more users is costly.

However, in this scenario, it is a "good problem" because it means your app is successful and you will have revenue for these expenses.

How to optimize fintech app development costs without sacrificing quality

With financial techniques, anyone can optimize the cost of development and lower the initial budget. Wavespace has been working on fintech app design since 2019. We’ve served 15+ industries (AI, SaaS, Fintech, Health) and our design work has contributed to over $10B in valuation.

Along the road, we’ve picked up industry insights (finance decisions) that will help fintech startups.

Here are the good financial decisions to save cash at the start.

Start with a Feature-Lean MVP

Don’t shoot for the moon. Don’t try to be PayPal on day one.

- Pick the one thing your fintech will do better than everyone else.

- Build that.

- Launch to the public.

- Get feedback.

- Then spend money adding more features.

A feature-lean MVP will prevent you from wasting money on building things that people don't use.

Use modular architecture

Don’t build the whole car in one day. Think of Lego blocks. Build features independently.

With modular architecture, if a block (chat feature) breaks. You can fix, update, or replace without breaking the whole app. Modular architecture makes future updates much faster & cheaper.

Invest in automated QA early

A few years back, developers had to manually test every screen to fine-tune the app. Now, developers can write "test scripts" that automatically check code every time after a save. This process finds bugs quickly and saves hundreds of hours of manual testing time.

Choose the right model

Fixed price: It is best, especially for MVPs.

- Fixed prices give you an advantage, and you know exactly what you want.

- You agree on an X amount, and you pay that X amount.

- Every other risk is on the developer.

Time and materials: Best for complex projects.

- You pay for the hours worked on the project.

- Hour-based projects give you the flexibility to change your mind.

- You need to be curious; it can be expensive if you are not careful.

Staff Augmentation: You hire a few (one or two) experts to join your team.

Bottom line

Building or designing & developing a fintech app in 2026 can cost a lot of money. It can cost from $30,000 to more than $350,000, depending on the features/abilities of the app.

Multiple things are the major players for this difference in price. It is because an app with more advanced AI features and security needs to follow strict compliance. And also, the location of development, financial regulation, and integrations with banks also drive up the cost.

However, a successful fintech app isn’t determined by how much money you have spent on it. It is determined by smart and strategic choices.

Wavespace suggests you start with a simple version of your app (MVP). Focus on your key features by making the app easy to use and slowly scale as you envisioned.

Frequently asked questions

Building a fintech app in 2026 usually takes 3 to 9+ months. A functioning MVP can be built in 2-4 months. And more advanced fintech with payments integrations, security, and compliance takes on average 6-12+ months. However, the time (month) depends on the complexity of the features you want.

Building for only one operating system costs less (either iOS or Android) than building two. Android apps can take a longer time (for optimization) because Android has thousands of phone models in the market. However, using frameworks like Flutter or React Native can save time.

Fintech apps handle sensitive information, such as money, personal information, and bank details. This is why fintech apps need much more security than an alarm app. An average fintech app needs stronger encryption, fraud detection, 2FA login, and compliance like PCI-DSS and KYC/AML. These things increase the cost of fintech development.

In 2026, a simple Fintech MVP to test your idea would cost around $30,000 to $70,000. However, this price can go up or down depending on the list of features.

MVP development is a quick service for startups. Minimum Viable Product is a simple working product before investing in the big picture. MVP is built with the most important features of a product. Startups build MVPs to check if their idea is working with their users. MVP services include product planning, designing, coding, testing, and guiding to launch.

The Rule of 200 is a business metric used for fintech companies. Simply put, if the fintech business metrics (growth, retention, and margins) don’t sum up to more than 200%, the business is not profitable.

More related blog

Have a Project? Let’s talk!

.avif)